How to Use This Calculator

Using our APY Calculator is simple. Here is a quick guide to help you calculate yields, compare options, and project your savings effectively.

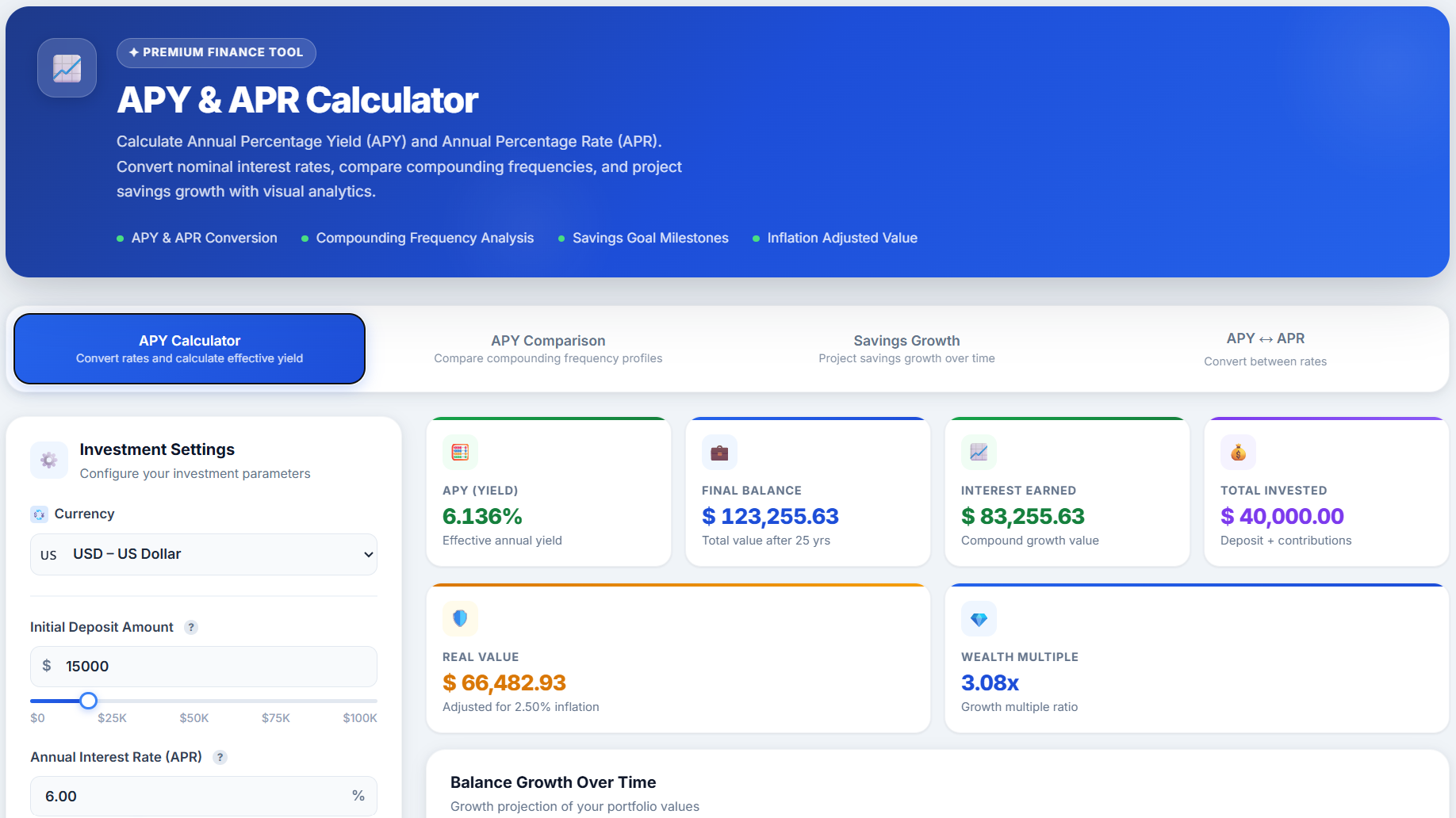

1 Configure Your Basic Inputs

Start by entering your financial details in the Calculator Mode. You can set your initial deposit, the nominal APR, and how often the interest is compounded (e.g., Monthly or Daily). You can also add regular contributions, specify your investment duration, and toggle inflation adjustments to see the real value of your future savings.

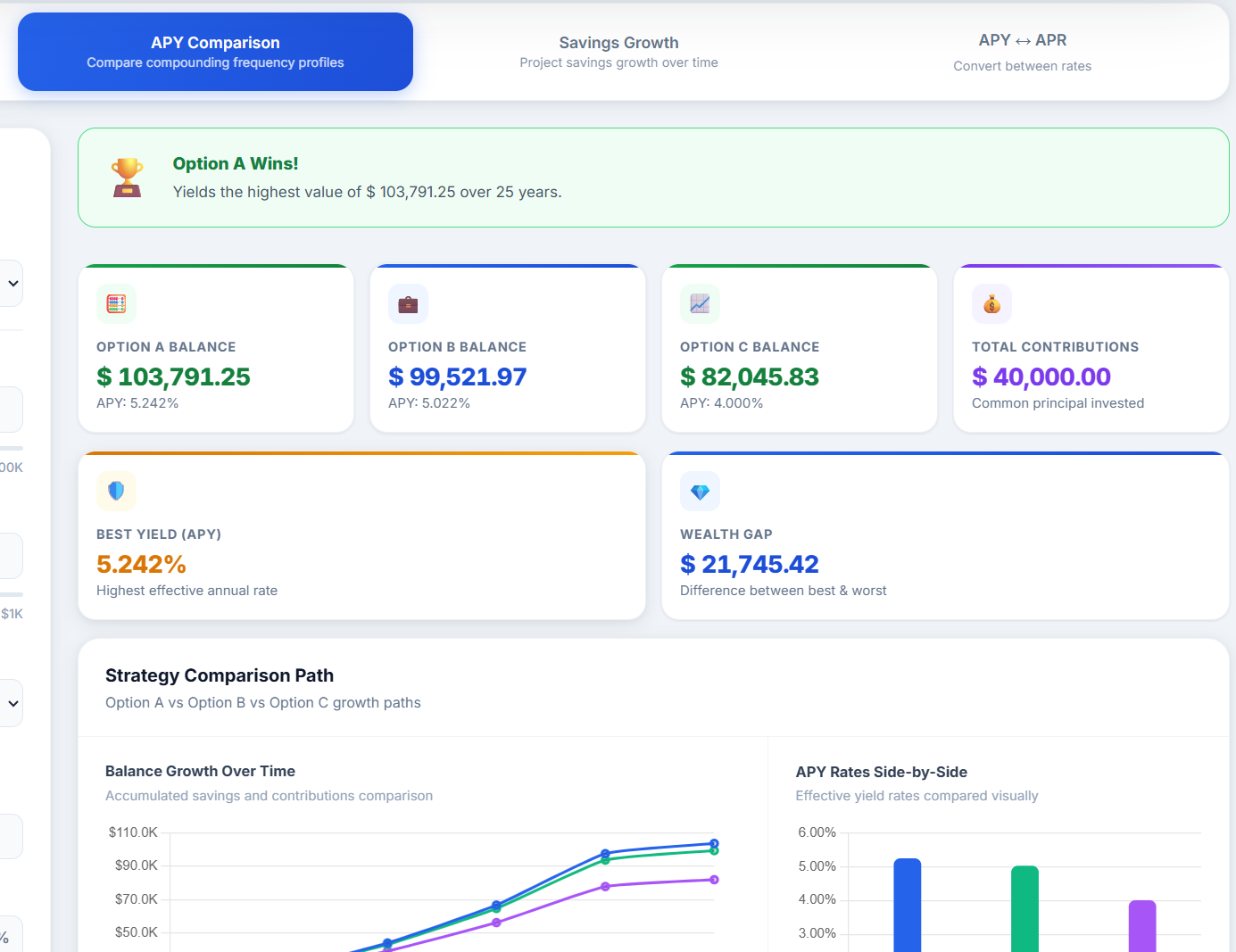

2 Compare Options Side-by-Side

Switch to the Comparison Mode if you want to evaluate up to three different investment options at once. Enter different APR rates and compounding frequencies (for example, comparing 5.12% compounded monthly against 4.90% compounded daily). The results panel will clearly show which option yields the highest return over time.

3 Analyze Your Results

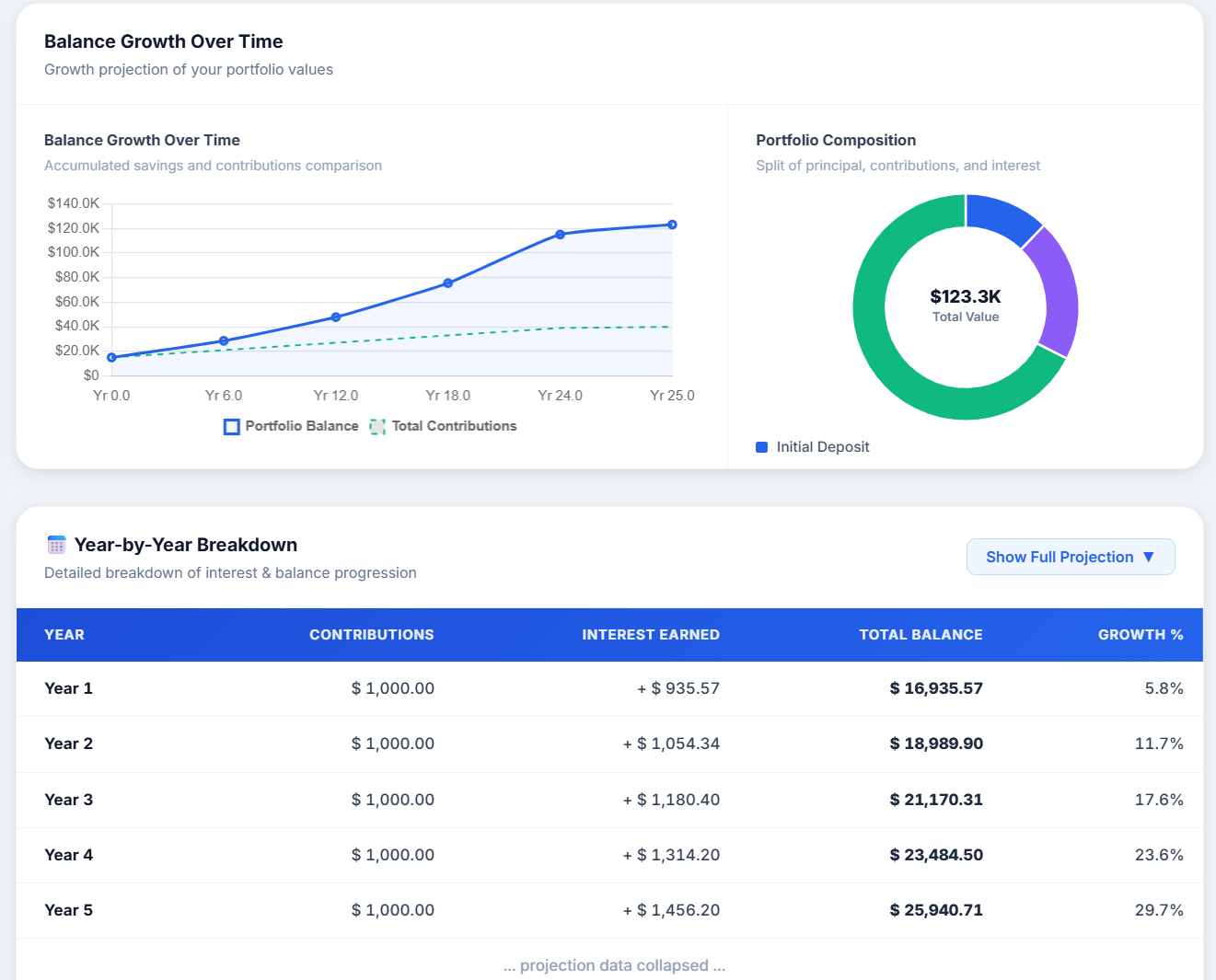

After calculation, the dashboard provides a full breakdown of your wealth accumulation. The result cards and charts display key metrics about your investment:

- Effective APY: The true annual yield after accounting for compounding.

- Total Future Value: The estimated final balance of your investment.

- Total Interest Earned: The pure profit generated from your principal and compounding.

- Inflation Adjusted Value: The real purchasing power of your final balance in today's money.

- Wealth Multiple: How many times your original total contributions have multiplied.

You can also use the interactive charts to visualize growth trajectories and view the detailed year-by-year projection table to track exactly how much you earn each period.

📚 APY vs APR — Complete Guide

What is APR? 📄

APR stands for Annual Percentage Rate — the nominal (stated) annual interest

rate on a financial product. It does not account for compounding within the year. Banks and

lenders typically advertise APR because it looks smaller and more attractive than APY. For example, a

loan advertised at 12% APR means 12% is the stated annual rate — but the true cost depends on how

frequently it compounds.

What is APY? 📈

APY stands for Annual Percentage Yield — the effective annual rate that

accounts for compounding. It tells you what you will actually earn (or pay) over a full year.

APY is always ≥ APR. The gap between them grows with higher rates and more frequent compounding. Savings

accounts and CDs in many countries are required by law to advertise APY so consumers see the real yield.

🔑 One-Line Rule: Use APY to compare savings products. Use APR to compare loan costs.

APY always tells the true story for investors.

Nominal vs Effective Rate 🧮

The nominal rate (APR) is what you see on the label. The effective rate

(APY/EAR) is what you actually get. The formula connecting them is:

APY = (1 + r/n)^n − 1 where r = APR (decimal), n = compounding

periods/year

Example: 10% nominal, compounded monthly → APY = (1 + 0.10/12)^12 − 1 = 10.47%. That

extra 0.47% is free money from compounding! 🎁

How Compounding Frequency Changes Everything 🔄

At the same nominal rate of 10%, here is how APY changes with frequency:

- 📅 Annually (n=1): APY = 10.00%

- 🗓️ Semi-Annual (n=2): APY = 10.25%

- 📆 Quarterly (n=4): APY = 10.38%

- 🌙 Monthly (n=12): APY = 10.47%

- ☀️ Daily (n=365): APY = 10.52%

As n approaches infinity (continuous compounding), APY approaches e^r − 1 = 10.517% at

10%. Practical

takeaway: daily vs monthly is a tiny difference; the rate matters far more than the compounding

frequency for typical savings scenarios. 💡

Daily vs Monthly Compounding — Real Numbers 💵

Let's invest 10,000 at 6% APR for 20 years under two scenarios:

- 📅 Monthly compounding: FV = 10,000 × (1 + 0.06/12)^(12×20) =

33,102

- ☀️ Daily compounding: FV = 10,000 × (1 + 0.06/365)^(365×20) =

33,198

Difference = only 96 over 20 years! This confirms that chasing "daily compounding" is

less important than securing a higher rate in the first place. A bank offering 6.1% APR monthly beats a

6% APR daily every time. 🏆

Bank Savings Account Example 🏦

Suppose Bank A offers 4.5% APY and Bank B offers 4.4% APR compounded

monthly. Which is better?

Bank B's APY = (1 + 0.044/12)^12 − 1 = 4.49%. So Bank A wins with 4.5% APY — even though

Bank B's APR sounds competitive. Always convert everything to APY before comparing. Our APR → APY

converter does this instantly! ⚡

Crypto Staking & High-Yield APY 🪙

Crypto platforms often advertise eye-catching APYs — 50%, 100%, even 200%. These figures are typically

calculated assuming the current reward rate holds for a full year and rewards are auto-compounded. In

reality:

- 🔻 Reward rates fluctuate daily based on network demand

- 📉 Token prices can drop, reducing real-world value

- ⏰ Lock-up periods may prevent withdrawal

- 🔒 Smart contract risk is real

⚠️ Crypto Warning: A 200% APY on a volatile token can still result in total loss if the

token price drops 90%. Always factor in price risk, not just yield.

Use this Future Value calculator to model crypto staking conservatively — plug in a fraction of

the advertised APY to stress-test your scenario.

How Inflation Reduces Your Real Return 📉

Even a great APY can be eaten by inflation. The real return formula is simple:

Real Return ≈ APY − Inflation Rate

If your savings account earns 5% APY but inflation is 4%, your real

purchasing-power gain is only ~1%. More precisely, Real Rate = (1 + APY) / (1 +

Inflation) − 1 (Fisher equation). Historically, many savings accounts have failed to beat inflation,

meaning savers are losing real wealth. Always check current inflation rates in your country and subtract

from your APY to find your true gain. 💸

🌍 Global Tip: In high-inflation economies (Argentina, Turkey, etc.), nominal interest

rates can be 40–80%, but real returns may still be negative if inflation runs higher. Always use real

return, not nominal APY, to judge investment quality.

Common Beginner Mistakes ❌

- ❌ Comparing APR to APY directly — always convert to same basis first

- ❌ Ignoring compounding frequency — two products with same APR can have different

APYs

- ❌ Forgetting taxes — after-tax APY = APY × (1 − tax rate); use post-tax figures

- ❌ Neglecting inflation — nominal yield ≠ real wealth growth

- ❌ Trusting crypto APY blindly — rates change hourly; past APY ≠ future APY

- ❌ Short time horizons — compounding is most powerful over 10+ year periods; don't

withdraw early

- ❌ Underestimating fees — a 0.5% annual management fee on a 5% APY product reduces

effective yield to only 4.5%

Quick Comparison: APR vs APY at a Glance 📊

| Feature |

APR |

APY |

| Accounts for compounding? |

❌ No |

✅ Yes |

| Better for comparing savings? |

❌ |

✅ Always use APY |

| Used by lenders to advertise? |

✅ Often lower-looking |

Sometimes |

| Formula |

r (nominal) |

(1+r/n)^n − 1 |

| Which is higher? |

— |

Always ≥ APR |

❓ Frequently Asked Questions

What is the difference between APR and APY? 🤔

▼

APR (Annual Percentage Rate) is the nominal rate — the number on the label, without

compounding. APY (Annual Percentage Yield) is the effective rate — what you actually earn after

compounding is applied. APY is always ≥ APR. The more frequently interest compounds, the bigger the

gap. Always compare APY for savings and APR for loans.

Why is APY always higher than or equal to APR? 📈

▼

Because compounding means you earn interest on previously earned interest. Each

compounding period adds a small amount to your principal, and the next period's interest is

calculated on this larger base. This snowball effect means the effective (APY) return always exceeds

the nominal (APR) rate — except when compounded once per year, where APY = APR.

How does daily compounding compare to monthly? ☀️

▼

Daily compounding (n=365) gives slightly more than monthly (n=12), but the difference

is very small in practice. On 10,000 at 6% for 10 years: monthly gives ~18,194, daily gives ~18,220.

The 26 difference is negligible. Focus on finding the highest APY rate, not obsessing over

compounding frequency.

What is the Effective Annual Rate (EAR)? 📐 ▼

EAR is another name for APY. It is the true annual interest rate accounting for

intra-year compounding. EAR = (1 + r/n)^n − 1. It is the most transparent metric for comparing

financial products with different compounding schedules. Regulators in many countries require banks

to disclose EAR/APY so consumers can compare fairly.

How does inflation affect my real return? 📉 ▼

Real Return ≈ APY − Inflation Rate. If your savings account pays 5% APY and inflation

runs at 3%, your real purchasing-power gain is approximately 2%. At 5% inflation, you are actually

losing real wealth even at 5% APY. Always look at real (inflation-adjusted) return when evaluating

long-term savings decisions.

What is the difference between nominal and effective

interest rate? 🔢 ▼

Nominal rate = the stated/advertised rate (APR), which ignores compounding. Effective

rate = the true annual yield after compounding (APY/EAR). A 6% nominal rate compounded monthly gives

an effective rate of 6.17%. Use the effective rate for any serious financial comparison.

How do I compare savings accounts from different banks? 🏦

▼

Always compare APY, not APR. APY standardises rates regardless of compounding

frequency. Use our APR → APY converter to convert any nominal rate to APY. Then compare APYs

directly. Also consider fees, minimum balance requirements, and deposit insurance. A slightly lower

APY with zero fees may beat a higher APY with monthly maintenance charges.

Is APY used in crypto staking? 🪙 ▼

Yes, crypto platforms advertise APY for staking. However, crypto APY is highly

volatile and often assumes rewards are auto-compounded at current rates. A 200% APY can drop to 5%

within weeks as more stakers join the pool. Additionally, token price drops can wipe out nominal

gains. Always model crypto APY conservatively and never invest more than you can afford to lose.

What compounding frequency is best for savers? 🗓️

▼

Daily compounding is theoretically best, but the practical difference vs monthly is

tiny. Far more important is maximising the actual APY rate offered. A 4.5% APY with monthly

compounding beats a 4.0% APY with daily compounding. Also check for fees, lock-up periods, and

FDIC/deposit insurance coverage.